The European steel sector emits roughly 5% of all EU greenhouse gas emissions, and over a quarter of industrial emissions. Sufficient demand for near-zero steel could unlock the industrial transformation needed to hit the EU climate targets. The report assesses 15 significant Nordic steel-buying companies and states that lack of private-sector demand is a major bottleneck in advancing sectoral climate goals.

Demand-side practices pose huge potential for climate impact

Despite current action lagging, existing best practices have the potential to triple demand for green steel. The report scores steel supply chains of major steel-buying companies on a scale from 0% to 100% to assess how compatible they are with keeping global temperatures below 1.5ºC. Scoring 100% would mean being fully compatible and thus using only near-zero emissions steel by 2040. Steel buyers currently score just 23% on average, but this could rise to 83% if existing best practices were adopted across companies.

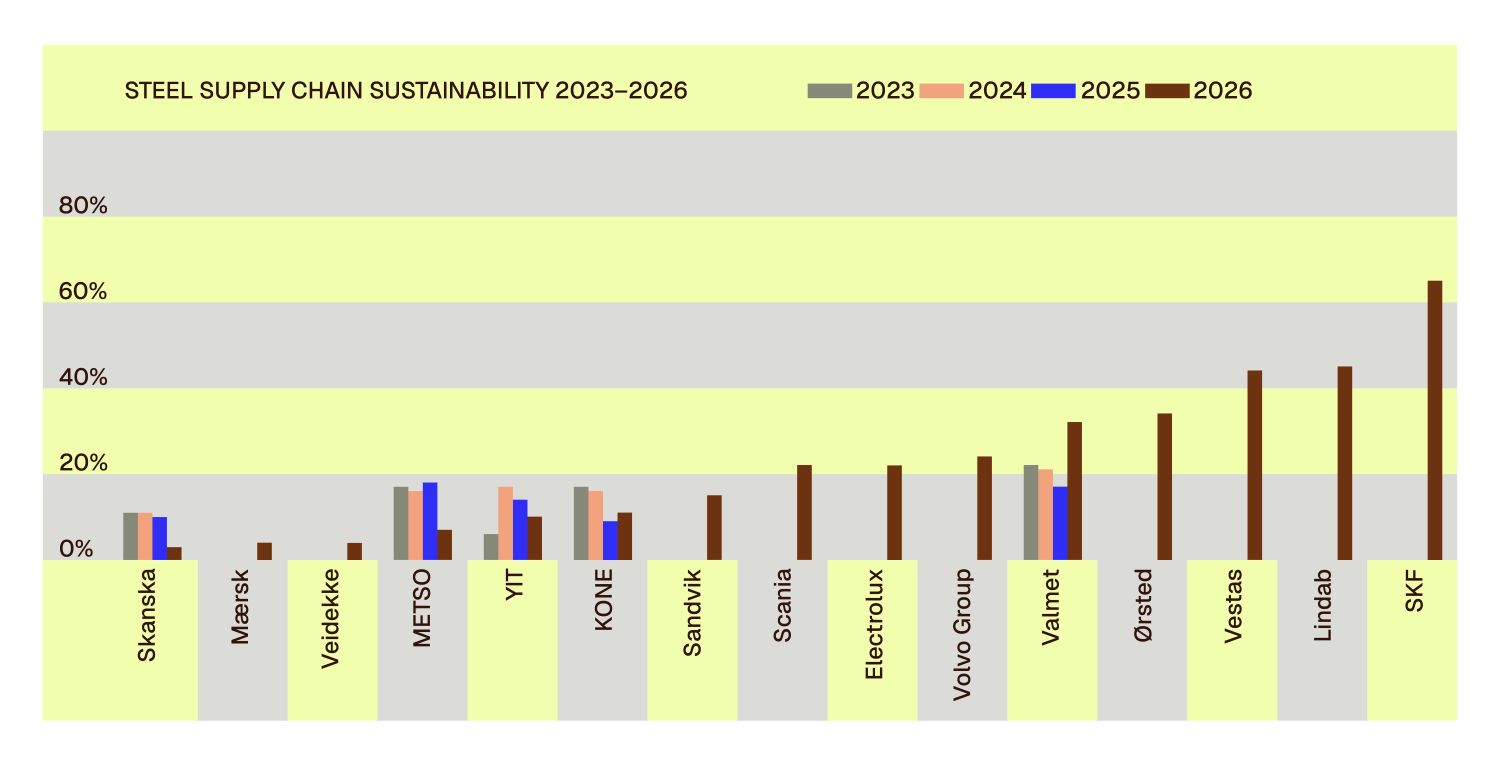

All 15 companies are publicly traded, operating in Finland, Sweden, Norway and Denmark and spanning sectors that consume large amounts of steel or have the potential to create lead markets for fossil‑free steel. The assessed companies are: SKF, Lindab, Vestas Wind Systems, Ørsted, Valmet, Volvo Group, Scania, Metso, Electrolux, Sandvik, Kone, A. P. Møller-Mærsk, YIT, Veidekke, and Skanska. The steel supply chain sustainability scores are illustrated in Figure 1 below, including scores from previous years, where applicable.

Figure 1. Companies’ Steel Supply Chain Sustainability scores, including a comparison to previous years, where applicable. On average, steel buyers are only 23% aligned with a pathway compatible with keeping global temperatures below 1.5ºC, but adopting already-existing best practices would bring them to 83% alignment.

Machinery firms outpace automakers in driving green steel demand

Machinery companies take the lead in creating demand for near-zero steel, even though the sector is not considered one of the most promising for lead market generation. The highest- scoring company is Swedish SKF, a global machinery company with over 38,000 staff, scoring 65% for its steel supply chain.

Steel is SKF’s most important raw material and the single largest contributor to our upstream carbon footprint. That makes decarbonising the steel value chain essential to achieving our net‑zero ambition by 2050. We do not see low‑carbon steel as a niche or premium option, but as a foundational industrial material that must scale rapidly, says Daniel Bosson, Group Circularity Manager at SKF.

Other relatively well-performing companies are Lindab, a machinery company employing roughly 5000 people, proving that also smaller actors have the power to influence steel producers; and Valmet, whose improvement is largely due to going through the process of creating a robust climate transition plan. The Danish wind energy companies Vestas and Ørsted perform well, too, proving that the renewable energy industry is already spearheading in lead market generation for fossil-free steel.

Industries most prominent for lead market generation for fossil‑free steel are automotive, construction, and whiteware companies. However, rather disappointingly, the companies representing the automotive industry—Volvo Group and Scania—although heavy vehicle manufacturers, perform only moderately well, with steel supply chain scores of 24% and 22%, respectively. Equally disappointing are the construction companies’ results: all three score below 20% for their steel supply chains. In addition, the only consumer‑facing company on the Scoreboard, Electrolux, achieves a disappointing score of 22% for its steel supply chain, despite the potential that consumer goods have for lead market generation for green steel.

Surprising country-level differences

The Nordic region’s exceptionally strong representation in the emerging fossil‑free steel industry gives local steel‑procuring companies added leverage to enter into binding offtake agreements and drive market demand for near‑zero‑emission steel. Swedish and Danish companies are already acting on this advantage, while Finnish and Norwegian companies lag behind. Securing such agreements now would position them among the first global buyers of fossil‑free steel, enabling them to take a leading role in climate action within the steel sector.

The disparity between countries is illustrated by the country-level steel supply chain average score: Denmark leads with 29%, Sweden is a close second with 28%, Finland third with 13%, and Norway last with only 4%.

Public procurement is not enough to create lead markets for green steel. Companies already have powerful tools at their disposal, but there is not enough incentive to use them, says Ninni Kähkönen, steel specialist at Just Shift.

The scorecard is available here.

About the Author

Just Shift is an independent civil society organisation campaigning for a 1.5°C-aligned steel sector by 2050 by influencing steel-procuring companies, public procurement, and institutional investors. This report is part of Just Shift’s work to push steel-procuring companies to shift steel demand from traditional coal-based iron and steelmaking to near-zero emission technologies. In addition to steel supply chains, the report evaluates the overall sustainability of the companies’ value chains.