David Leitch writes on the Renew Economy website about the impact of the construction boom underway in China. Worryingly, not only is construction driving an increase coal fired electricity, but China’s share of oil and gas consumption is also rising. While we are aware of the efforts that China is doing in the energy transition, so much more needs to be done.

The grim reality about China ‘s building boom and coal burning

China is where 28 per cent of global fossil fuel CO2 emissions take place and they are going up. A rough guesstimate of 5% increase this year, or more, is on the cards.

Not only is construction driving an increase coal fired electricity, but China’s share of oil and gas consumption is also rising. China at a 58% share totally dominates global cement consumption, the 4th largest driver of emissions.

The simple fact is that whether it’s fair or unfair, the world needs China to do more. We don’t see things improving until the construction boom ends and that won’t be this year.

China’s economy has big implications for everyone

Even on GDP China’s economy is easily the second largest in the world at US$12 trillion compared to the USA $19 trillion and 2.5X Japan in Number 3 place at $4.8 trillion . But in heavy industry China is the dominant world power.

For electricity decarbonization China is far more important than the USA. Some context is provided in figures 1.

And shown as a graph in figure 2.

You don’t need to be Warren Buffet to know that most cement (the 4th largest contributor to CO2 emissions after coal, gas and oil) and lots of steel and aluminium go into construction. More than half the world’s construction takes place in China and when it does it pushes up electricity consumption which pushes up coal consumption and CO2 output.

Despite producing over 3.5 bt of coal China is a net importer, and those imports effectively drive the world price for coal.

Those statistics are why we regard construction in China, along with the USA 10 year bond rate, as the two key global variables.

It’s China’s emissions stupid

China’s share of global fossil fuel emissions at 28% is held down relative to its coal share because of its lower (but growing) share of oil and gas consumption. Notwithstanding cumulative contributions, per capita data, or any other way of cutting the data, the basic fact remains that the extent of global warming depends on China’s emission control, or lack of it, more than any other single factor.

National electricity policies may be counteracted by provincial policy

Most media focusses on national policy. Here in Australia it’s what the Federal Govt does, or in the USA what Trump is doing, or in China, to the extent that there is media coverage, on the National Chinese Government policy. Still this understandable national focus often means insufficient attention on what is going one one level down.

In Australia, Victorian and Queensland policy is now more important than Federal policy. In the USA what’s happening in California is completely at odds with USA national policy and the same could be said of several other States.

In China it turns out that despite national Chinese rules trying to limit the building of new coal power plants there are still over 250 GW under construction encouraged by Chinese provincial govts.

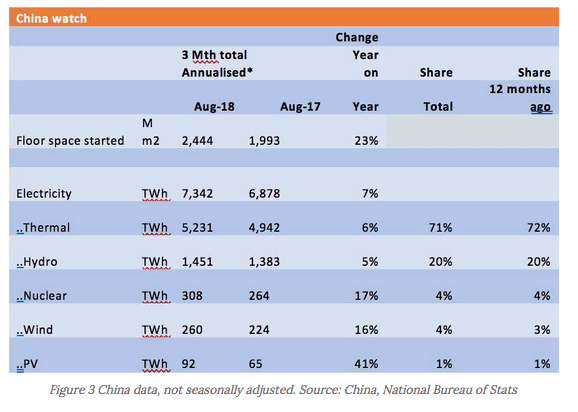

The data scoreboard in China

Note that the monthly real estate started is not reported directly. What is reported is the monthly annual total for the year to date. We get the monthly number by subtracting prior month total from current month total.

What the data shows is that the real estate boom in China remains in full swing. This will lead to growth in use of construction materials such as cement and steel and to higher electricity consumption.

Could we be bothered we could do a diffusion index to show the overall manufacturing situation, but hey, ask your friendly investment bank.

Here we just note that output of lithium batteries (big and small) is growing 10% year on year.

The data also shows growth of thermal electricity of 6% year on year and this has several consequences:

- It’s an ongoing train wreck for global warming and one day push will come to shove in China. Eventually global warming could feed into an international imperative capable of causing conflict. We are not there yet in the global public opinion stakes.

- It’s keeping coal prices high. That’s good news for renewables developers everywhere.

- It will provide a profit incentive in China for the developers of the new coal plant. They will see that their capacity utilization can be high enough to justify ongoing construction. Message: You can’t rely on current market conditions in China to slow down coal fuelled electricity plant construction. Quite the reverse. This brings us to:

The CoalSwarm monitor

CoalSwarm is as a very interesting global effort to track coal fuelled electricity plant construction. Every plant over 30 MW under construction around the entire world is monitored. Even the USA Govt. would have had trouble doing this 15 years ago, but with today’s technology a small global team is able to do a great job.

In September CoalSwarm reported that 259 GW of new capacity remains under active development in China despite a series of central Govt orders obstentially aimed at trying to slow down or stop the plants being developed.

Either the central Chinese authorities didn’t mean what they said, or they don’t have the power to enforce their rules, or both. Which ever way you cut it, these new plants are a problem for global warming control efforts.

CoalSwarm notes that permitting of these plants occurred largely in 2015 when permitting authority was transferred to provinces in September 2014.

We note that even CoalSwarm’s data doesn’t include “captive coal plants” . These are plants notionally dedicated to and owned by a user, eg an aluminium smelter. Global attention on these is increasing as its increasingly clear they have avoided national rules.

China has 981 GW of coal plant at the end of 2017 and a notional target of 1100 GW. Obviously with 260 GW under construction that target will likely be exceeded by at least 5%.

How do we know these plants are still being built?

The true advantage of CoalSwarm’s technology based approach to monitoring these plants is the use of daily satellite records from Planet.

Planet has over 130 satellites in orbit today and can image anywhere on earth daily at 3 meter and 72 centimeter resolution.

I had to have a valium and a good lie down when I read this. It’s truly incredible. And its only going to increase.

Want to know what competitor brick inventories look like? Get an image. Want to know how the new Tesla factory is going? Get an image.

Want to know how much rain forest has been destroyed, or how much new land is devoted to sugar cane in Brazil? Get an image.

Who needs Pine Gap? Totally out of date, or soon will be.

Planet has the world’s largest constellation of Earth-imaging satellites, with new ones being launched every 3-4 months. Thus the technology in the satellite improves quickly. Modern software allows images to be downloaded to Google Cloud so customers get fast access.

In this case CoalSwarm has been able to track progress of the 260 GW of permitted coal plant in China.

Hope springs eternal – China’s kite flying 35% renewables by 2030

Here at ITK we take the view that when investors want to make money longer term from electricity, gas its best to give more weight to carbon emissions than less.

Coal profits are through the roof because China has restricted its own coal ouput. If things go on this way that won’t last. China will either cut coal demand or increase coal output. Even if it increases coal ouput that won’t last for more than a year or two either. Eventuallly global warming pressures will make meaningful policy come to the fore.

Even in China, coincidentally just after the CoalSwarm report the NDRC has disclosed a draft policy, conveniently sighted by Bloomberg that proposes a 35% reneweable target by 2030.

This sounds wonderful but as Fig 3 above shows, if we treat Hydro and nuclear as renewable resources, then China is already at 29%.

Unfortunately beyond an initial article by Bloomberg reposted by many others, few details of the draft policy are in the public domain.